Feature Story 1 What is the “realization of No. 1 value-added productivity”?

SDGs to which we contribute and why we should contribute to SDGs

We will contribute to achieving the Target-8 goals by building a system that enables the employees to work with high motivation, maximize the added value, and also maximize the return to the stakeholders.

In our medium- to long-term business plan called NEXT10 “Change!”, starting in 2019, the 100th anniversary of our foundation, we set the three strategic pillars as “productivity reform,” “company-wide promotion of ‘de-construction’ business activities,” and “internal reform.” Giving immediate top priority to “productivity reform,” and declaring a priority policy for the final fiscal year (fiscal 2027) as “realization of No. 1 value-added productivity,” MAEDA has set a new “added value” unique to MAEDA, and has been working to maximize it.

This feature story explains what MAEDA’s unique “added value” is, and introduces our efforts to determine how we will maximize the added value.

Background against which MAEDA has come to set a unique added value

In the future environment surrounding the construction industry, the finances of the national and local governments are expected to become tighter due to reduced tax revenues resulting from population decline, and an increase of social security-related costs due to the progress of aging. In the meantime, social infrastructures will become deteriorated at almost the same time. Therefore, not only construction of new infrastructures, but also investment in the maintenance and management or updating of existing infrastructures are estimated not to proceed as intended. In addition, given that further aggravation of the shortage of bearers due to a decline in the productive-age population resulting from a declining birthrate and an aging population, and that shifting to digitalization is inevitable, it is considered that the conventional value will also change in the construction industry and that the industrial structure itself will change.

To ensure that the whole Group grows lastingly under such circumstances, MAEDA has defined the ideal form we seek in the medium to long term as a “general infrastructure service company,” which manages the infrastructure operation from the upstream to the downstream. To achieve this, a system that encourages all stakeholders including the community, company, employees, and shareholders to advance toward a single goal will be needed. We have come to think that, for this purpose, it is important that all of the elements, such as contribution to society, sales and profits of the company, salaries of the employees, and return to shareholders, work with each other and spiral upward, not each of these elements individually improving, and that it is important to set a unique added value in order to achieve this.

A unique added value that MAEDA defines

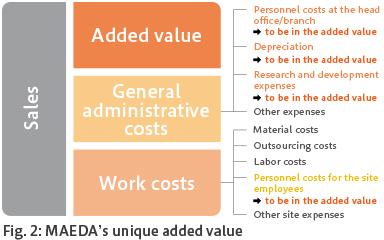

MAEDA’s unique added value is defined as the sum of operating profit, total personnel expenses, depreciation, and research and development expenses, as shown in the formula below. In other words, it is the difference calculated by subtracting work costs (consisting of material costs, outsourcing costs, labor costs, and other site expenses excluding personnel costs for site employees), which is external expenditure incurred in the work, and general administrative costs (consisting of personnel costs, depreciation, and other expenses excluding research and development expenses), from the sales of the whole company, as shown in Fig. 2.

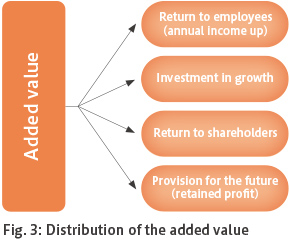

As shown in Fig. 3, our policy for the added value is to distribute it to the return to employees, investment in growth, return to shareholders, and provision for the future (retained profit) in a well-balanced manner. Increasing the amounts distributed to these four areas to the extent possible will lead to improving our corporate value. Therefore, we are seeking to maximize the added value, which will serve as its funding source.

Mechanism of added value maximization

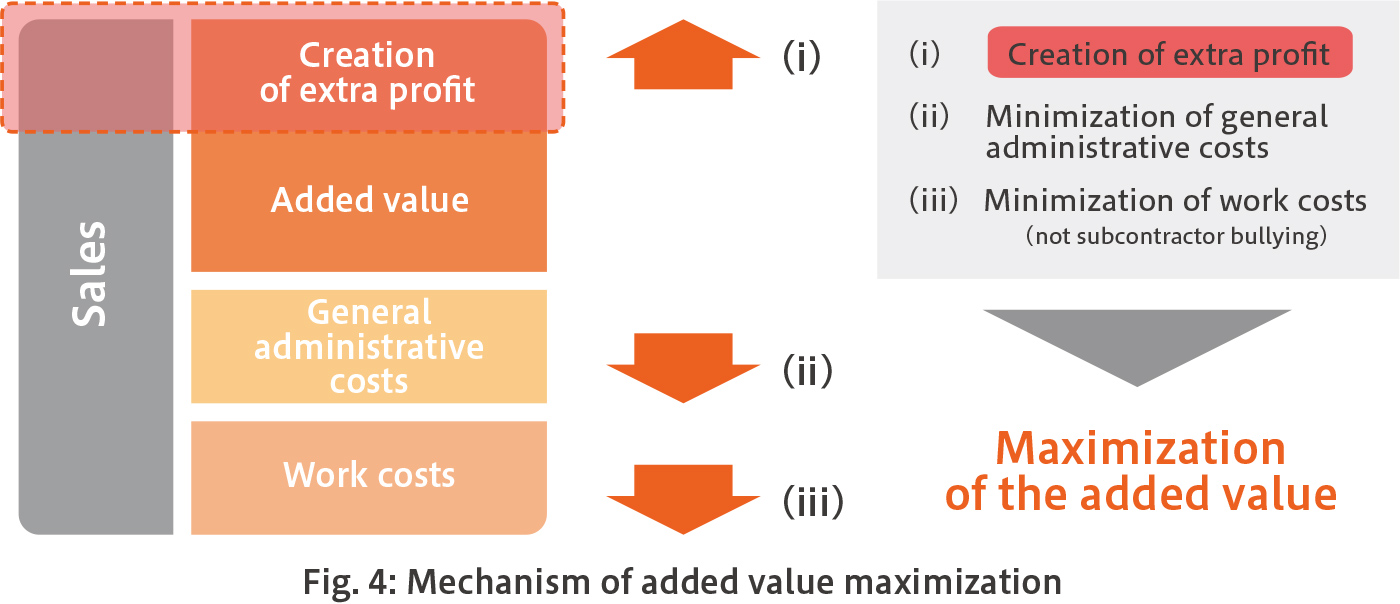

To maximize the added value, minimization of work costs and general administrative costs will be the minimum approach required, as shown in Fig. 4. However, there is a limit to this, and, therefore, “creation of extra profit” will be needed. To create this extra profit, creation of a higher-value-added business from the viewpoint of a business proprietor in upstream areas such as planning, designing, and procurement, and downstream areas such as maintenance management, operation, and renovation, instead of sticking only to existing contracted works, will be a major element for achieving this goal. This is exactly the practicing of CSV management, in which MAEDA is to find problems that the community and customers have, and solve them in cooperation with them.

MAEDA’s unique added value

“Continuing to raise the employees’ motivation” is the key to maximizing the added value

To maximize the distributed amounts including investment in growth and return to shareholders, most important of all, it is essential to maximize the added value, which will serve as its funding source.

To maximize the added value, creation of extra profit will be needed in addition to minimizing the work costs and general administrative costs. This is easy to say, but is a difficult task to actually accomplish. Taking the minimization of the work costs as an example, subcontractor bullying is outrageous, and, in the light of minimizing costs while raising their added value, achieving this will require considerable effort to improve work productivity. In addition, the creation of extra profit will require ideas, thoughts, and actions beyond the conventional stereotypes, and, therefore, considerable awareness reform for working on a new area will be essential. Considering what is needed to overcome these barriers, we have come to think that helping all employees to feel job satisfaction and keep raising their motivation toward their work will be an important key to answering the question, and that the starting point for this is in “returning profit back to employees.” In short, this means returning profit back to employees in the form of remuneration according to the created added value. Based on this way of thinking, for bonuses, we introduced a transparency-ensuring system in fiscal 2020, which includes adopting a calculation standard according to the added value and disclosing it to all employees. We are convinced that turning these efforts into raising of motivation of employees will achieve maximization of the added value, which will then “spiral upward” to investment in growth and further return to shareholders.

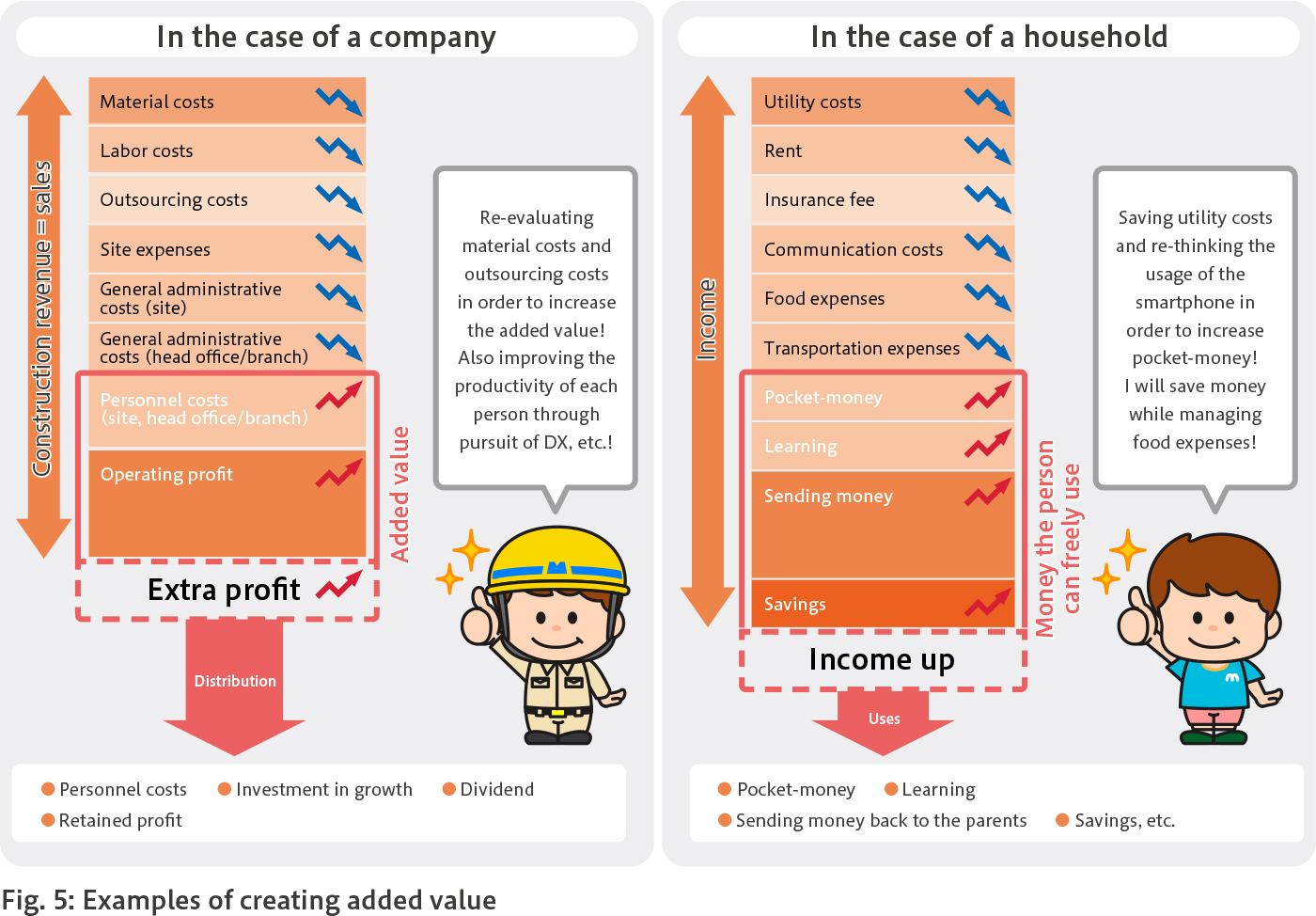

Considering the added value in a household budget

The mechanism of increasing the added value is similar to managing a household budget (Fig. 5). For example, if external expenditures such as utility costs and communication costs are reduced, the amount of money that the person can freely use will increase in return. The person can use that money for uses intended to raise his/her value such as for learning or as pocket-money.

MAEDA intends to review its external expenditures such as material costs and outsourcing costs in a manner similar to this. And we think that the added value that has been increased through such an approach will be distributed to the return to employees, investment in growth, return to shareholders, and provision for the future (retained profit), which will then increase the corporate value. Reduction of external expenditures is one of the means to increase the added value. However, the essence of the added value increase is “adding new value.” Therefore, it will be important to create extra profit as a result of “adding new value to the service by solving problems of the community and customers.”

How to maximize the added value

The above has explained how to raise added value. If simply the maximization of added value is pursued, the purpose may be achieved by increasing the number of employees and increasing the labor time. However, in such a case, the amount of returned profit for each employee may be reduced, and, therefore, the question arises on what the maximization effort should be for in the first place, and the result would be “wagging the dog.” What is important is to maximize added value with fewer employees and less labor time. For this reason, MAEDA has adopted “value-added productivity,” in which the total labor time of employees is the denominator and the added value is the numerator, as shown in the formula below, as a management index, and has been controlling this index.

As stated in the beginning, “realization of No. 1 value-added productivity” is a priority policy of “productivity reform,” which is immediate top priority among the three strategic pillars of our medium- to long-term business plan called NEXT10. However, the remaining two pillars, “company-wide promotion of de-contacting business activities” and “internal reform” are also essential elements for improving value-added productivity.

As stated above, to maximize the added value, which is the numerator of value-added productivity, reduction of work costs and general administrative costs, excluding personnel costs, and creation of extra profit will be needed. However, unless stable and high-earning businesses are increased in the first place, the effect of these efforts will be limited. Our businesses such as PPP/PFI, concession business, and renewable energy business, which MAEDA has worked on under our strategy, “company-wide promotion of de-contacting business activities,” have stably created high added values, and will substantially contribute to added value maximization. Therefore, we will continue to work on them. In addition, we aim to create more added values by encouraging all employees to move on with their work from the viewpoint of a business proprietor based on a “de-construction” mentality.

Furthermore, we are pursuing the minimization of total labor time of employees, which is the denominator of added-value productivity, under the “internal reform” strategy. “Internal reform” consists of “awareness reform” and “system reform.” “Awareness reform” is intended to reduce labor time by pursuing waste elimination, personnel-saving, and labor-saving through internal reform of the conventional ways of working. For “system reform,” in fiscal 2019, we introduced a new personnel system intended to enable efforts of employees including the reduction of labor time to be rewarded, based on the thought that it is important that each and every employee keeps trying new things and develops into a stronger individual. Using “system reform” by means of introducing a new personnel system as the driver, we aim to build a corporate structure/culture that enables us to address any change in the medium to long term by seeking “awareness reform.”